Is 2026 a Good Time to Buy a Home in Connecticut?

Is Now Still a Good Time to Buy a Home in Connecticut? 2026 Data Says Yes.

If you are renting in Connecticut and wondering whether 2026 is a good time to buy, you are not alone. The headlines can feel confusing, but the numbers tell a clear, encouraging story: for many Connecticut renters and first-time buyers, waiting is actually getting more expensive, not less.

The Waiting Game Myth: Prices Are Not Dropping in Connecticut

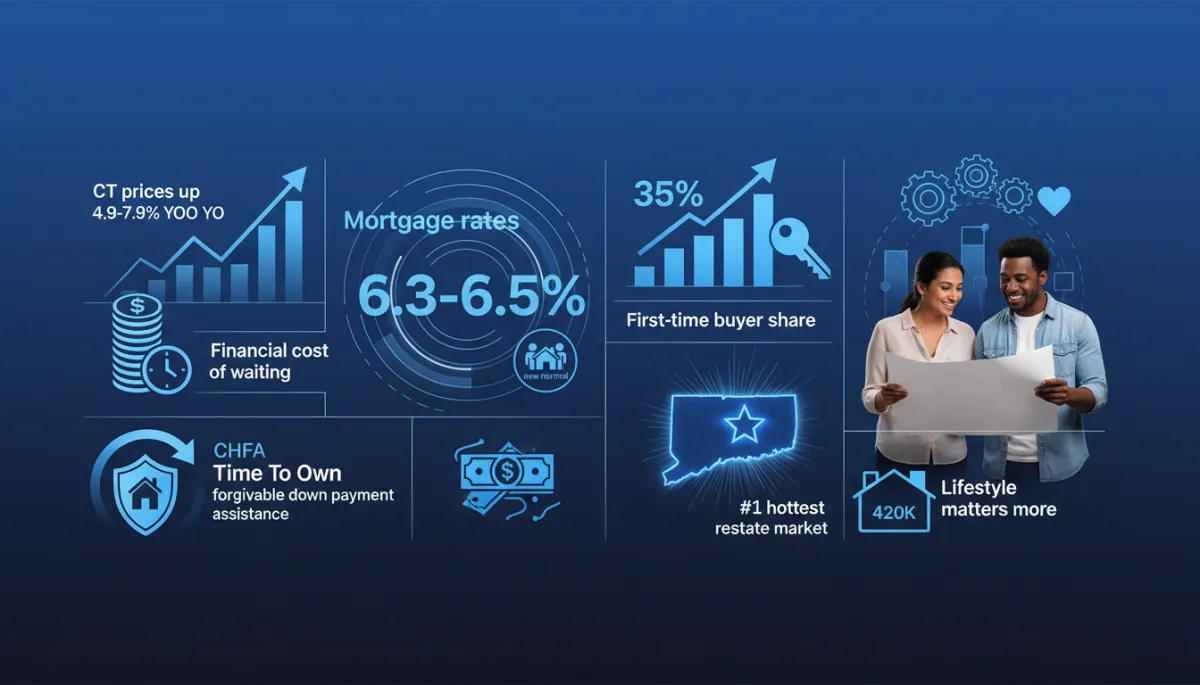

A common belief among renters is, “I’ll just wait for prices to come down.” In much of the country, and especially here, that strategy has not worked. Recent reports from major portals like Redfin and Zillow show Connecticut home values are still climbing, up roughly 4.9% to 7.9% year-over-year, depending on the source and area you look at. That lines up with statewide data showing steady 3–5% annual gains and even higher jumps in hot pockets like Hartford County and parts of the shoreline.

At the same time, supply remains tight. Connecticut has only about two months of inventory in many markets—far below the 5–6 months considered balanced. According to the Office of the State Comptroller and local MLS data, homes are still selling around or above list price. In other words, the Connecticut housing market is not behaving like a market that is about to crash; it is behaving like a market with strong, ongoing demand.

The Real Cost of Waiting: A $20,000 Penalty in Just 12 Months

To see how waiting plays out in dollars, imagine a typical Connecticut home priced at $400,000 today. With a modest 5% annual appreciation—less than some of the recent year-over-year gains—that same home would cost $420,000 in 12 months. That is a $20,000 increase for the exact same property, before you even factor in potential changes in mortgage rates or closing costs.

For a renter or first-time buyer, that extra $20,000 is essentially a penalty for waiting. It might mean a higher monthly payment, a larger required down payment, or being priced out of the neighborhood you really want. Meanwhile, you are still paying rent—helping your landlord build equity instead of building your own long-term wealth in the Connecticut housing market.

Mortgage Rates: 6.3–6.5% Is Becoming the New Normal

Another reason some buyers stay on the sidelines is mortgage rates. As of late June 2026, Connecticut’s average 30-year fixed rate is hovering around 6.3%–6.5%, according to NerdWallet and MonitorBankRates. That is higher than the ultra-low pandemic rates, but it is also lower than many feared a year ago—and relatively stable.

Lawrence Yun, Chief Economist for the National Association of Realtors (NAR), has called rates above 6% the “new normal” that consumers are increasingly accepting. Buyers across the country are realizing that waiting for 3% or 4% rates to magically return is not a realistic plan. Instead, they are moving forward with today’s rates, knowing they can always refinance later if and when rates move down.

Demand Is Releasing: First-Time Buyers Are Stepping In

One of the clearest signs that 2026 is a good time to buy a home in Connecticut is who is actually buying. Nationally, the first-time buyer share hit 35% in May 2026, the highest level since June 2020. That surge tells us that a lot of pent-up demand—especially from younger, diverse, and long-time renter households—is finally coming off the sidelines and into homeownership.

Here in Connecticut, that trend is amplified by our local strength. Recent rankings from Zillow and Construction Coverage place Connecticut as the #1 hottest real estate market in the country, with the Hartford metro ranked #1 nationally. That means more people are choosing to put down roots here, and they are willing to compete for the limited homes available. Getting in sooner rather than later positions you to benefit from that ongoing demand instead of chasing it.

Connecticut’s hot market rewards buyers who act early instead of waiting on the sidelines.

CHFA “Time To Own” Forgivable Down Payment Assistance: Powerful Help for First-Time Buyers

The good news is you do not have to do this alone. For qualified first-time buyers, the Connecticut Housing Finance Authority (CHFA) still offers the Time To Own forgivable down payment assistance program—one of the most generous in the country. Eligible buyers can receive up to 20% of the home price for down payment plus up to 5% for closing costs, all at 0% interest.

Over time, that assistance can be forgiven as long as you meet the program requirements and stay in the home. For many Connecticut renters, CHFA down payment assistance is the missing puzzle piece that turns “someday” into “this year.” If saving 20% down has felt impossible, this is a concrete, data-backed way to bridge the gap and step into homeownership in 2026.

Lifestyle Timing vs. Market Timing: When Life Calls, It’s Worth Listening

While the numbers are important, your life matters more than trying to outsmart the market. Maybe you are welcoming a new baby, blending households, tired of rent hikes, working from home more, or simply ready for a backyard of your own. Those lifestyle shifts are powerful signals that it may be the right time to buy a home in Connecticut 2026, regardless of whether rates tick up or down a quarter point next month.

History shows that buyers who purchase when their life calls for it—and hold their homes for the long term—tend to come out ahead. You lock in your housing costs, build equity, and create stability for yourself and the people you care about, whether that is family, friends, or community. Market timing is hard to get perfect. Life timing is much clearer.

Ready to Explore Your Options? Connect with MelindaTheRealtor

If you are curious about whether now is a good time to buy Connecticut real estate for you, the next step is a personalized conversation. Every situation is different—credit, savings, rent, commute, family needs—and good guidance should be tailored, not generic.

Reach out to me today! Call me at 860-784-7214 for a free consultation. Never too busy for you to be my #1 client!

Together, we will review the latest Connecticut housing market data, your budget, and programs like CHFA down payment assistance so you can make a confident, informed decision in 2026.

FAQ: Buying a Home in Connecticut in 2026

1. Is 2026 really a good time to buy a home in Connecticut, or should I keep renting?

Based on current data, 2026 is still a good time to buy Connecticut real estate for many households. Prices are rising 4.9–7.9% year-over-year, inventory is tight, and Connecticut is ranked the hottest market in the country. Continuing to rent while prices and rents both climb often costs more over time than buying a well-chosen home and building equity. The key is making sure the numbers work for your budget and time horizon.

2. What if mortgage rates drop after I buy?

With rates around 6.3–6.5% and NAR’s Lawrence Yun calling above-6% the “new normal,” it is wise to plan using today’s rates. If rates fall in the future, you can often refinance to lower your payment. If prices continue to rise, you also gain from the appreciation while you wait. Many buyers are deciding that the risk of waiting—and paying more for the same home later—is higher than the risk of buying now and refinancing later.

3. How do I know if I qualify for CHFA Time To Own assistance?

Eligibility for CHFA Time To Own depends on factors like income limits, purchase price caps, your status as a first-time buyer, and where in Connecticut you are buying. Because the program can provide up to 20% down plus 5% closing costs at 0% interest—and is forgivable over time—it is worth exploring early in your planning. I regularly connect clients with CHFA-approved lenders who can review your situation and confirm whether you qualify, often in just a short phone call.

Sources

Connecticut Housing Finance Authority (CHFA) – Time To Own Down Payment Assistance

https://www.chfa.org/homebuyers-homeowners/homebuyers/time-to-own/

Official information on Connecticut's Time To Own forgivable down payment assistance program, including eligibility requirements, loan amounts, and program guidelines for first-time homebuyers.National Association of REALTORS® (NAR) – Research & Statistics

https://www.nar.realtor/research-and-statistics

Provides national housing market reports, existing-home sales data, affordability trends, first-time buyer statistics, and economic forecasts from NAR Chief Economist Lawrence Yun.Zillow Research – Connecticut Housing Market

https://www.zillow.com/home-values/state/ct/

Offers current Connecticut home value trends, annual appreciation rates, housing forecasts, and local market insights used to evaluate statewide housing conditions.Redfin Data Center – Connecticut Housing Market

https://www.redfin.com/news/data-center/

Provides up-to-date Connecticut housing market statistics, including median sale prices, inventory levels, days on market, and year-over-year market trends.NerdWallet – Current Mortgage Interest Rates

https://www.nerdwallet.com/mortgages/mortgage-rates

Tracks current national mortgage interest rates and market trends, helping buyers understand financing costs and compare rate movements over time.